Following the launch of Namebase’s registry, a major barrier to Handshake market participation was removed. Prior to this, only a handful of top-level domain (TLD) owners were able to sell subdomains (second-level domains, or SLDs). Through the registry, participation has skyrocketed – currently 582 Handshake TLDs are listed on Encirca. Thanks to Twitter user @HandshakeSLDs, fantastic and granular data regarding SLD sales is now available to the public.

This post uses @HandshakeSLDs’s ‘SLD Report for May 2021’ as the basis for back-of-envelope analysis that annualizes May performance and extrapolates proceeds to owners and resultant yields. The back-of-envelope aspect should be emphasized, as this exercise required many simplifications. Notably, besides .c, these TLDs have short sales track records, so it is unclear if May performance will be representative of longer trends.

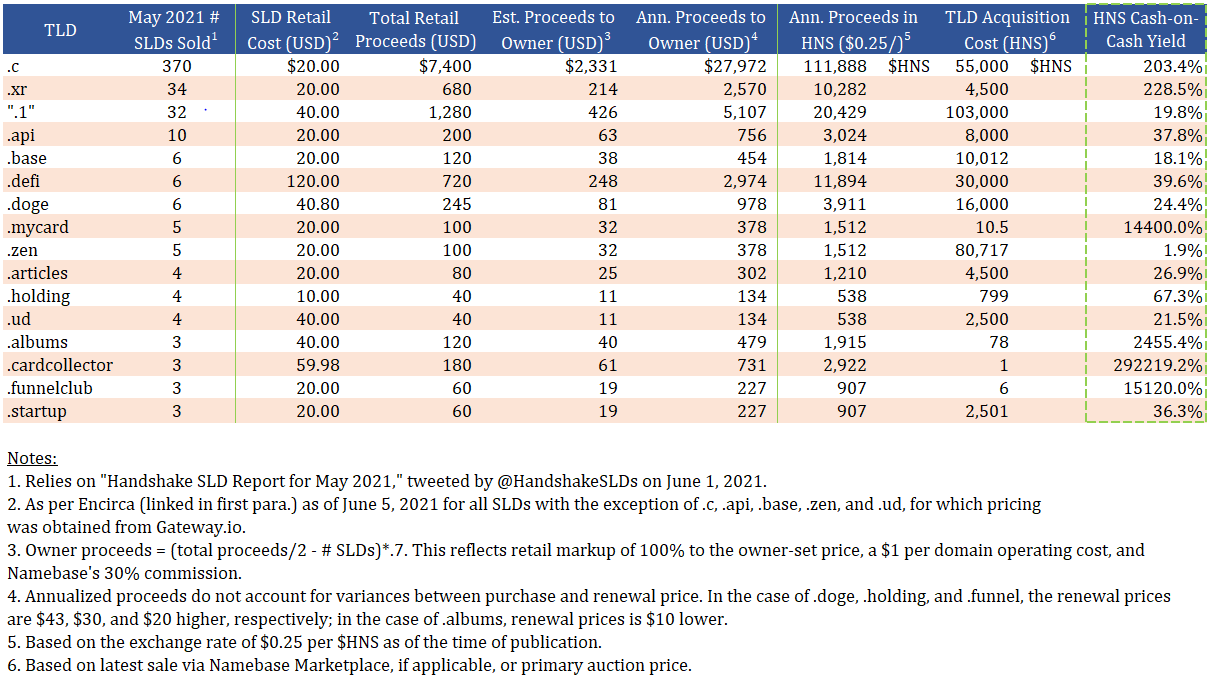

The table below summarizes May SLD sales, estimates proceeds net of commissions to the owner, annualizes that amount, and then converts US dollars (USD) to $HNS in order to derive a cash-on-cash yield (in $HNS terms) based on each TLD’s acquisition cost.

At this time, the yields calculated above should be taken with a grain of salt. However, excluding TLDs acquired for less than 100 $HNS (.mycard, .albums, .cardcollector, and .funnelclub), a somewhat cohesive grouping of the other TLDs emerge, with .c and .xr ahead of the pack, and .zen behind. .c is clearly the market leader, with the volume to show it. .xr had strong sales, though only two more than .1, and at half the price; its yield is boosted by its low acquisition cost. .zen suffers from low sales volume relative to its high cost, conditions that should be surmountable given the TLD’s mass appeal and brevity.

Given the ability to purchase SLDs in USD at a fixed cost, yields calculated in $HNS terms are highly sensitive to the HNS/USD exchange rate. Here, yield reacts inversely to $HNS price. For instance, changing the price of $HNS to $0.75 in the above analysis decreases .c’s and .xr’s yields to 67.8% and 76.2%, respectively. Of course, none of these calculated yields consider the costs of the $HNS each owner used to purchase these TLDs, which are unknown.

In subsequent posts and as more data becomes available, this blog aims to expand this snapshot of May into meaningful exploration of trends over time.

**CORRECTION: The original version of this post relied on discounted pricing for the .c, .api, .base, and .zen TLDs that understated the estimated proceeds to their owners. The above table and relevant commentary have been corrected to reflect that nuance.

DISCLAIMER AND DISCLOSURE

This commentary is not intended to be investment advice. Please consult appropriate investment, financial planning, legal and tax professionals regarding any investment decisions. The author, as a hobbyist, has owned, owns, and plans to own in the future numerous TLDs, as well as $HNS; has engaged in numerous transactions to acquire and dispose of the same; and plans to engage in similar transactions in the future. The author may purchase or sell SLDs in the future.